Questões de Concurso

Comentadas para analista (superior)

Foram encontradas 11.236 questões

Resolva questões gratuitamente!

Junte-se a mais de 4 milhões de concurseiros!

Ano: 2012

Banca:

CEFET-BA

Órgão:

CREF - 13ª Região (BA-SE)

Provas:

CEFET-BA - 2012 - CREF - 13ª Região (BA-SE) - Analista Advogado

|

CEFET-BA - 2012 - CREF - 13ª Região (BA-SE) - Analista Agente de Orientação e Fiscalização |

CEFET-BA - 2012 - CREF - 13ª Região (BA-SE) - Analista Contador |

Q503588

Noções de Informática

Existem diversas formas de acesso a uma caixa postal de e-mails. Aplicativos como o OutLook da Microsoft competem diretamente com o acesso a portais de WebMail.

Comparando-se as duas soluções, a alternativa que apresenta uma vantagem do OutLook frente a um portal de WebMail é a

Comparando-se as duas soluções, a alternativa que apresenta uma vantagem do OutLook frente a um portal de WebMail é a

Ano: 2012

Banca:

CEFET-BA

Órgão:

CREF - 13ª Região (BA-SE)

Provas:

CEFET-BA - 2012 - CREF - 13ª Região (BA-SE) - Analista Advogado

|

CEFET-BA - 2012 - CREF - 13ª Região (BA-SE) - Analista Agente de Orientação e Fiscalização |

CEFET-BA - 2012 - CREF - 13ª Região (BA-SE) - Analista Contador |

Q503586

Noções de Informática

Na elaboração de documentos usando o Microsoft Word, muitas vezes, é necessário copiar trechos de textos disponíveis na Internet. Em alguns casos, no entanto, os textos encontram-se formatados de forma específica e, ao copiá-los, os formatos da página Web são aplicados também no documento do Word.

Para resolver esse problema, mantendo a formatação originalmente adotada no Microsoft Word, é correto afirmar:

Para resolver esse problema, mantendo a formatação originalmente adotada no Microsoft Word, é correto afirmar:

Ano: 2012

Banca:

CEFET-BA

Órgão:

CREF - 13ª Região (BA-SE)

Provas:

CEFET-BA - 2012 - CREF - 13ª Região (BA-SE) - Analista Advogado

|

CEFET-BA - 2012 - CREF - 13ª Região (BA-SE) - Analista Agente de Orientação e Fiscalização |

CEFET-BA - 2012 - CREF - 13ª Região (BA-SE) - Analista Contador |

Q503585

Noções de Informática

Na navegação em uma página de um banco, deve-se adotar alguns procedimentos associados à segurança do usuário.

Identifique com V os procedimentos verdadeiros e com F, os falsos

( ) Não se deve utilizar links para a página do banco contido em e-mail, mesmo que ele tenha sido aparentemente enviado pelo banco e recebido em sua caixa postal.

( ) É recomendável verificar se a figura de um cadeado aparece na tela do navegador durante o acesso, pois essa figura indica que o tráfego entre o computador e a instituição financeira está sendo criptografado.

( ) É necessário garantir a instalação e atualização constante de um antivírus de boa qualidade no computador utilizado.

A alternativa que contém a sequência correta, de cima para baixo, é a

Identifique com V os procedimentos verdadeiros e com F, os falsos

( ) Não se deve utilizar links para a página do banco contido em e-mail, mesmo que ele tenha sido aparentemente enviado pelo banco e recebido em sua caixa postal.

( ) É recomendável verificar se a figura de um cadeado aparece na tela do navegador durante o acesso, pois essa figura indica que o tráfego entre o computador e a instituição financeira está sendo criptografado.

( ) É necessário garantir a instalação e atualização constante de um antivírus de boa qualidade no computador utilizado.

A alternativa que contém a sequência correta, de cima para baixo, é a

Ano: 2012

Banca:

CEFET-BA

Órgão:

CREF - 13ª Região (BA-SE)

Provas:

CEFET-BA - 2012 - CREF - 13ª Região (BA-SE) - Analista Advogado

|

CEFET-BA - 2012 - CREF - 13ª Região (BA-SE) - Analista Agente de Orientação e Fiscalização |

CEFET-BA - 2012 - CREF - 13ª Região (BA-SE) - Analista Contador |

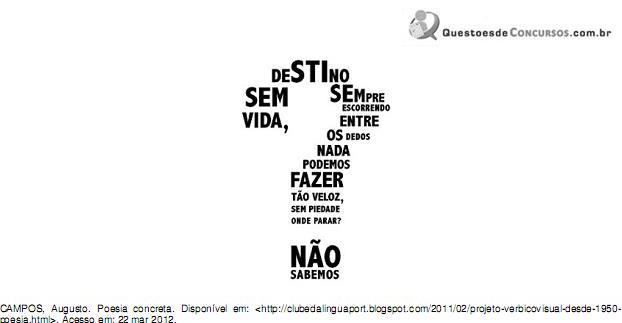

Q503582

Português

A leitura e a análise do poema concretista permitem afirmar que

Ano: 2013

Banca:

CESPE / CEBRASPE

Órgão:

BACEN

Provas:

CESPE - 2013 - BACEN - Analista - Gestão e Análise Processual

|

CESPE - 2013 - BACEN - Analista - Conhecimentos Básicos - Áreas 1, 2, 4 e 5 |

CESPE - 2013 - BACEN - Analista - Análise e Desenvolvimento de Sistemas |

CESPE - 2013 - BACEN - Analista - Política Econômica e Monetária |

CESPE - 2013 - BACEN - Analista - Contabilidade e Finanças |

Q484786

Inglês

Texto associado

Recent corporate collapses, such as EBS International and Société Générale, have brought about renewed scrutiny into corporate governance mechanisms. Given the pervasiveness of Information Technology (IT) in many organizations, the examination of corporate governance mechanisms also includes IT governance mechanisms. IT governance is defined as “a structure of relationships and processes to direct and control the enterprise in order to achieve the enterprise’s goals by adding value while balancing risk versus return over IT and its processes”.

In light of increased public awareness, professional bodies such as the Information Systems Audit and Control Association (ISACA) have undertaken a number of steps to provide guidance in the implementation of effective IT governance. The approach taken by ISACA appears to be largely based upon two concepts. The first concept relates to increasing the awareness of issues and concepts relating to IT governance in the public domain. The second concept involves the provision of guidelines and the identification of best-practice IT governance mechanisms. Interestingly, the effectiveness of these best-practice mechanisms in improving IT governance is largely based upon conceptual arguments. As such, it becomes important to ascertain if these best-practice mechanisms do impact upon the level of IT governance.

As IT escalates in terms of importance and pervasiveness in the operations of firms, it is inexorably tied to specific mechanisms that are prescribed for good corporate governance, most notably, a sound system of internal controls. Accordingly, effective IT governance is a critical underpinning for a system of good corporate governance that minimizes agency losses for a firm.

Internet: < http://onlinelibrary.wiley.com > (adapted).

Based on the text above, judge the following item.

In light of increased public awareness, professional bodies such as the Information Systems Audit and Control Association (ISACA) have undertaken a number of steps to provide guidance in the implementation of effective IT governance. The approach taken by ISACA appears to be largely based upon two concepts. The first concept relates to increasing the awareness of issues and concepts relating to IT governance in the public domain. The second concept involves the provision of guidelines and the identification of best-practice IT governance mechanisms. Interestingly, the effectiveness of these best-practice mechanisms in improving IT governance is largely based upon conceptual arguments. As such, it becomes important to ascertain if these best-practice mechanisms do impact upon the level of IT governance.

As IT escalates in terms of importance and pervasiveness in the operations of firms, it is inexorably tied to specific mechanisms that are prescribed for good corporate governance, most notably, a sound system of internal controls. Accordingly, effective IT governance is a critical underpinning for a system of good corporate governance that minimizes agency losses for a firm.

Internet: < http://onlinelibrary.wiley.com > (adapted).

Based on the text above, judge the following item.

In spite of the pervasiveness of IT in many organizations, it is essential for enterprises to balance risks and detect fraud.

Ano: 2013

Banca:

CESPE / CEBRASPE

Órgão:

BACEN

Provas:

CESPE - 2013 - BACEN - Analista - Conhecimentos Básicos - Áreas 1, 2, 4 e 5

|

CESPE - 2013 - BACEN - Analista - Análise e Desenvolvimento de Sistemas |

CESPE - 2013 - BACEN - Analista - Política Econômica e Monetária |

CESPE - 2013 - BACEN - Analista - Contabilidade e Finanças |

Q484785

Inglês

Texto associado

Recent corporate collapses, such as EBS International and Société Générale, have brought about renewed scrutiny into corporate governance mechanisms. Given the pervasiveness of Information Technology (IT) in many organizations, the examination of corporate governance mechanisms also includes IT governance mechanisms. IT governance is defined as “a structure of relationships and processes to direct and control the enterprise in order to achieve the enterprise’s goals by adding value while balancing risk versus return over IT and its processes”.

In light of increased public awareness, professional bodies such as the Information Systems Audit and Control Association (ISACA) have undertaken a number of steps to provide guidance in the implementation of effective IT governance. The approach taken by ISACA appears to be largely based upon two concepts. The first concept relates to increasing the awareness of issues and concepts relating to IT governance in the public domain. The second concept involves the provision of guidelines and the identification of best-practice IT governance mechanisms. Interestingly, the effectiveness of these best-practice mechanisms in improving IT governance is largely based upon conceptual arguments. As such, it becomes important to ascertain if these best-practice mechanisms do impact upon the level of IT governance.

As IT escalates in terms of importance and pervasiveness in the operations of firms, it is inexorably tied to specific mechanisms that are prescribed for good corporate governance, most notably, a sound system of internal controls. Accordingly, effective IT governance is a critical underpinning for a system of good corporate governance that minimizes agency losses for a firm.

Internet: < http://onlinelibrary.wiley.com > (adapted).

Based on the text above, judge the following item.

In light of increased public awareness, professional bodies such as the Information Systems Audit and Control Association (ISACA) have undertaken a number of steps to provide guidance in the implementation of effective IT governance. The approach taken by ISACA appears to be largely based upon two concepts. The first concept relates to increasing the awareness of issues and concepts relating to IT governance in the public domain. The second concept involves the provision of guidelines and the identification of best-practice IT governance mechanisms. Interestingly, the effectiveness of these best-practice mechanisms in improving IT governance is largely based upon conceptual arguments. As such, it becomes important to ascertain if these best-practice mechanisms do impact upon the level of IT governance.

As IT escalates in terms of importance and pervasiveness in the operations of firms, it is inexorably tied to specific mechanisms that are prescribed for good corporate governance, most notably, a sound system of internal controls. Accordingly, effective IT governance is a critical underpinning for a system of good corporate governance that minimizes agency losses for a firm.

Internet: < http://onlinelibrary.wiley.com > (adapted).

Based on the text above, judge the following item.

Internal control is a central issue on corporate governance.

Ano: 2013

Banca:

CESPE / CEBRASPE

Órgão:

BACEN

Provas:

CESPE - 2013 - BACEN - Analista - Gestão e Análise Processual

|

CESPE - 2013 - BACEN - Analista - Conhecimentos Básicos - Áreas 1, 2, 4 e 5 |

CESPE - 2013 - BACEN - Analista - Análise e Desenvolvimento de Sistemas |

CESPE - 2013 - BACEN - Analista - Política Econômica e Monetária |

CESPE - 2013 - BACEN - Analista - Contabilidade e Finanças |

Q484784

Inglês

Texto associado

Recent corporate collapses, such as EBS International and Société Générale, have brought about renewed scrutiny into corporate governance mechanisms. Given the pervasiveness of Information Technology (IT) in many organizations, the examination of corporate governance mechanisms also includes IT governance mechanisms. IT governance is defined as “a structure of relationships and processes to direct and control the enterprise in order to achieve the enterprise’s goals by adding value while balancing risk versus return over IT and its processes”.

In light of increased public awareness, professional bodies such as the Information Systems Audit and Control Association (ISACA) have undertaken a number of steps to provide guidance in the implementation of effective IT governance. The approach taken by ISACA appears to be largely based upon two concepts. The first concept relates to increasing the awareness of issues and concepts relating to IT governance in the public domain. The second concept involves the provision of guidelines and the identification of best-practice IT governance mechanisms. Interestingly, the effectiveness of these best-practice mechanisms in improving IT governance is largely based upon conceptual arguments. As such, it becomes important to ascertain if these best-practice mechanisms do impact upon the level of IT governance.

As IT escalates in terms of importance and pervasiveness in the operations of firms, it is inexorably tied to specific mechanisms that are prescribed for good corporate governance, most notably, a sound system of internal controls. Accordingly, effective IT governance is a critical underpinning for a system of good corporate governance that minimizes agency losses for a firm.

Internet: < http://onlinelibrary.wiley.com > (adapted).

Based on the text above, judge the following item.

In light of increased public awareness, professional bodies such as the Information Systems Audit and Control Association (ISACA) have undertaken a number of steps to provide guidance in the implementation of effective IT governance. The approach taken by ISACA appears to be largely based upon two concepts. The first concept relates to increasing the awareness of issues and concepts relating to IT governance in the public domain. The second concept involves the provision of guidelines and the identification of best-practice IT governance mechanisms. Interestingly, the effectiveness of these best-practice mechanisms in improving IT governance is largely based upon conceptual arguments. As such, it becomes important to ascertain if these best-practice mechanisms do impact upon the level of IT governance.

As IT escalates in terms of importance and pervasiveness in the operations of firms, it is inexorably tied to specific mechanisms that are prescribed for good corporate governance, most notably, a sound system of internal controls. Accordingly, effective IT governance is a critical underpinning for a system of good corporate governance that minimizes agency losses for a firm.

Internet: < http://onlinelibrary.wiley.com > (adapted).

Based on the text above, judge the following item.

IT governance mechanisms contribute toward an increased level of overall effective IT governance.

Ano: 2013

Banca:

CESPE / CEBRASPE

Órgão:

BACEN

Provas:

CESPE - 2013 - BACEN - Analista - Gestão e Análise Processual

|

CESPE - 2013 - BACEN - Analista - Conhecimentos Básicos - Áreas 1, 2, 4 e 5 |

CESPE - 2013 - BACEN - Analista - Análise e Desenvolvimento de Sistemas |

CESPE - 2013 - BACEN - Analista - Política Econômica e Monetária |

CESPE - 2013 - BACEN - Analista - Contabilidade e Finanças |

Q484783

Inglês

Texto associado

Recent corporate collapses, such as EBS International and Société Générale, have brought about renewed scrutiny into corporate governance mechanisms. Given the pervasiveness of Information Technology (IT) in many organizations, the examination of corporate governance mechanisms also includes IT governance mechanisms. IT governance is defined as “a structure of relationships and processes to direct and control the enterprise in order to achieve the enterprise’s goals by adding value while balancing risk versus return over IT and its processes”.

In light of increased public awareness, professional bodies such as the Information Systems Audit and Control Association (ISACA) have undertaken a number of steps to provide guidance in the implementation of effective IT governance. The approach taken by ISACA appears to be largely based upon two concepts. The first concept relates to increasing the awareness of issues and concepts relating to IT governance in the public domain. The second concept involves the provision of guidelines and the identification of best-practice IT governance mechanisms. Interestingly, the effectiveness of these best-practice mechanisms in improving IT governance is largely based upon conceptual arguments. As such, it becomes important to ascertain if these best-practice mechanisms do impact upon the level of IT governance.

As IT escalates in terms of importance and pervasiveness in the operations of firms, it is inexorably tied to specific mechanisms that are prescribed for good corporate governance, most notably, a sound system of internal controls. Accordingly, effective IT governance is a critical underpinning for a system of good corporate governance that minimizes agency losses for a firm.

Internet: < http://onlinelibrary.wiley.com > (adapted).

Based on the text above, judge the following item.

In light of increased public awareness, professional bodies such as the Information Systems Audit and Control Association (ISACA) have undertaken a number of steps to provide guidance in the implementation of effective IT governance. The approach taken by ISACA appears to be largely based upon two concepts. The first concept relates to increasing the awareness of issues and concepts relating to IT governance in the public domain. The second concept involves the provision of guidelines and the identification of best-practice IT governance mechanisms. Interestingly, the effectiveness of these best-practice mechanisms in improving IT governance is largely based upon conceptual arguments. As such, it becomes important to ascertain if these best-practice mechanisms do impact upon the level of IT governance.

As IT escalates in terms of importance and pervasiveness in the operations of firms, it is inexorably tied to specific mechanisms that are prescribed for good corporate governance, most notably, a sound system of internal controls. Accordingly, effective IT governance is a critical underpinning for a system of good corporate governance that minimizes agency losses for a firm.

Internet: < http://onlinelibrary.wiley.com > (adapted).

Based on the text above, judge the following item.

The Information Systems Audit and Control Association have advised against a number of steps concerning the implementation of effective IT governance.

Ano: 2013

Banca:

CESPE / CEBRASPE

Órgão:

BACEN

Provas:

CESPE - 2013 - BACEN - Analista - Gestão e Análise Processual

|

CESPE - 2013 - BACEN - Analista - Conhecimentos Básicos - Áreas 1, 2, 4 e 5 |

CESPE - 2013 - BACEN - Analista - Análise e Desenvolvimento de Sistemas |

CESPE - 2013 - BACEN - Analista - Política Econômica e Monetária |

CESPE - 2013 - BACEN - Analista - Contabilidade e Finanças |

Q484782

Inglês

Texto associado

Recent corporate collapses, such as EBS International and Société Générale, have brought about renewed scrutiny into corporate governance mechanisms. Given the pervasiveness of Information Technology (IT) in many organizations, the examination of corporate governance mechanisms also includes IT governance mechanisms. IT governance is defined as “a structure of relationships and processes to direct and control the enterprise in order to achieve the enterprise’s goals by adding value while balancing risk versus return over IT and its processes”.

In light of increased public awareness, professional bodies such as the Information Systems Audit and Control Association (ISACA) have undertaken a number of steps to provide guidance in the implementation of effective IT governance. The approach taken by ISACA appears to be largely based upon two concepts. The first concept relates to increasing the awareness of issues and concepts relating to IT governance in the public domain. The second concept involves the provision of guidelines and the identification of best-practice IT governance mechanisms. Interestingly, the effectiveness of these best-practice mechanisms in improving IT governance is largely based upon conceptual arguments. As such, it becomes important to ascertain if these best-practice mechanisms do impact upon the level of IT governance.

As IT escalates in terms of importance and pervasiveness in the operations of firms, it is inexorably tied to specific mechanisms that are prescribed for good corporate governance, most notably, a sound system of internal controls. Accordingly, effective IT governance is a critical underpinning for a system of good corporate governance that minimizes agency losses for a firm.

Internet: < http://onlinelibrary.wiley.com > (adapted).

Based on the text above, judge the following item.

In light of increased public awareness, professional bodies such as the Information Systems Audit and Control Association (ISACA) have undertaken a number of steps to provide guidance in the implementation of effective IT governance. The approach taken by ISACA appears to be largely based upon two concepts. The first concept relates to increasing the awareness of issues and concepts relating to IT governance in the public domain. The second concept involves the provision of guidelines and the identification of best-practice IT governance mechanisms. Interestingly, the effectiveness of these best-practice mechanisms in improving IT governance is largely based upon conceptual arguments. As such, it becomes important to ascertain if these best-practice mechanisms do impact upon the level of IT governance.

As IT escalates in terms of importance and pervasiveness in the operations of firms, it is inexorably tied to specific mechanisms that are prescribed for good corporate governance, most notably, a sound system of internal controls. Accordingly, effective IT governance is a critical underpinning for a system of good corporate governance that minimizes agency losses for a firm.

Internet: < http://onlinelibrary.wiley.com > (adapted).

Based on the text above, judge the following item.

Although considerable research has been devoted to IT governance, rather less attention has been paid to corporate governance mechanisms.

Ano: 2015

Banca:

FCC

Órgão:

SEFAZ-PI

Prova:

FCC - 2015 - SEFAZ-PI - Analista do Tesouro Estadual - Conhecimentos Específicos |

Q476947

Administração Financeira e Orçamentária

A despesa bruta de pessoal do Poder Executivo de determinado Estado da federação, ao final do exercício, era de R$ 22.750.000,00. Na apuração da despesa líquida de pessoal, ou, seja, na verificação dos limites, de acordo com a Lei Complementar no 101/2000, NÃO serão computadas, entre outras, as despesas referentes a

Ano: 2015

Banca:

FCC

Órgão:

SEFAZ-PI

Prova:

FCC - 2015 - SEFAZ-PI - Analista do Tesouro Estadual - Conhecimentos Específicos |

Q476934

Administração Financeira e Orçamentária

No mês de janeiro de 2015, determinado ente da federação contabilizou receitas orçamentárias, no valor total de R$ 22.350.000,00. Quanto ao impacto na situação líquida patrimonial, as receitas podem ser efetivas e não efetivas. São consideradas como efetivas e não efetivas, respectivamente, as receitas referentes a

Ano: 2015

Banca:

FCC

Órgão:

SEFAZ-PI

Prova:

FCC - 2015 - SEFAZ-PI - Analista do Tesouro Estadual - Conhecimentos Específicos |

Q476928

Direito Constitucional

Acerca dos orçamentos previstos na Constituição Federal, é correto afirmar que

Ano: 2015

Banca:

FCC

Órgão:

SEFAZ-PI

Prova:

FCC - 2015 - SEFAZ-PI - Analista do Tesouro Estadual - Conhecimentos Específicos |

Q476925

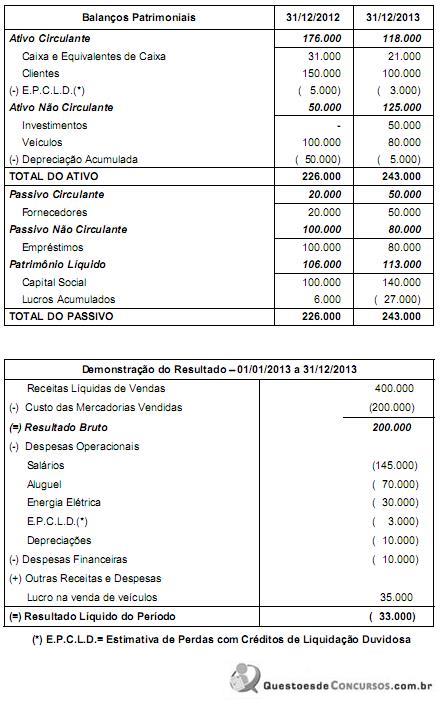

Contabilidade Geral

Os Balanços Patrimoniais da Empresa Internacional S.A. em 31/12/2012 e 31/12/2013 e a Demonstração do Resultado para o

ano de 2013 são apresentados a seguir (valores em reais):

Informações Adicionais:

- Os investimentos são avaliados pelo Método de Custo.

- Todos os veículos existentes em 31/12/2012 foram vendidos em 30/06/2013. A taxa de depreciação destes bens era 10% ao ano.

- O aumento de capital foi efetuado com a entrega de veículos no valor de R$ 20.000,00 e o restante em dinheiro.

- Os empréstimos existentes em 31/12/2012 foram integralmente pagos em 01/01/2013.

- As despesas financeiras são pagas no próprio período a que competem. A empresa classifica os pagamentos de juros como operacionais.

O valor correspondente ao caixa gerado pelas Atividades Operacionais no ano de 2013 foi, em reais:

Informações Adicionais:

- Os investimentos são avaliados pelo Método de Custo.

- Todos os veículos existentes em 31/12/2012 foram vendidos em 30/06/2013. A taxa de depreciação destes bens era 10% ao ano.

- O aumento de capital foi efetuado com a entrega de veículos no valor de R$ 20.000,00 e o restante em dinheiro.

- Os empréstimos existentes em 31/12/2012 foram integralmente pagos em 01/01/2013.

- As despesas financeiras são pagas no próprio período a que competem. A empresa classifica os pagamentos de juros como operacionais.

O valor correspondente ao caixa gerado pelas Atividades Operacionais no ano de 2013 foi, em reais:

Ano: 2015

Banca:

FCC

Órgão:

SEFAZ-PI

Prova:

FCC - 2015 - SEFAZ-PI - Analista do Tesouro Estadual - Conhecimentos Específicos |

Q476912

Contabilidade Geral

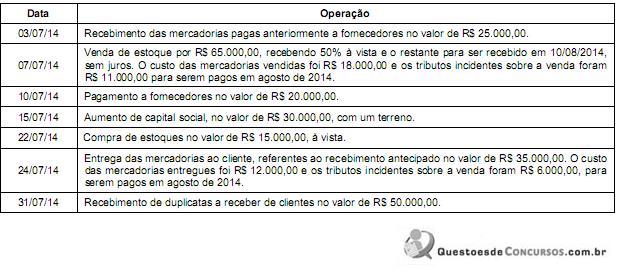

A Cia. Piauí S.A. possuía em 30/06/2014 a seguinte situação patrimonial:

− Caixa e Equivalentes de Caixa: ..................................................................................... R$ 50.000,00

− Duplicatas a Receber de Clientes: ................................................................................R$ 120.000,00

− Adiantamentos a Fornecedores: .................................................................................... R$ 25.000,00

− Fornecedores a pagar: .................................................................................................. R$ 60.000,00

− Adiantamentos de Clientes: ........................................................................................... R$ 35.000,00

− Capital Social: ............................................................................................................... R$ 100.000,00

Durante o mês de julho de 2014 a Cia. Piauí S.A. realizou as seguintes operações:

Após o registro das operações acima, o valor total do ativo da Cia. Piauí S.A. em 31/07/14 era, em reais,

− Caixa e Equivalentes de Caixa: ..................................................................................... R$ 50.000,00

− Duplicatas a Receber de Clientes: ................................................................................R$ 120.000,00

− Adiantamentos a Fornecedores: .................................................................................... R$ 25.000,00

− Fornecedores a pagar: .................................................................................................. R$ 60.000,00

− Adiantamentos de Clientes: ........................................................................................... R$ 35.000,00

− Capital Social: ............................................................................................................... R$ 100.000,00

Durante o mês de julho de 2014 a Cia. Piauí S.A. realizou as seguintes operações:

Após o registro das operações acima, o valor total do ativo da Cia. Piauí S.A. em 31/07/14 era, em reais,

Ano: 2015

Banca:

FCC

Órgão:

SEFAZ-PI

Prova:

FCC - 2015 - SEFAZ-PI - Analista do Tesouro Estadual - Conhecimentos Específicos |

Q476909

Conhecimentos Bancários

De acordo com as contas do Balanço de Pagamentos, a Necessidade de Financiamento Externo - NFE é obtida por meio

Ano: 2015

Banca:

FCC

Órgão:

SEFAZ-PI

Prova:

FCC - 2015 - SEFAZ-PI - Analista do Tesouro Estadual - Conhecimentos Específicos |

Q476901

Administração Financeira e Orçamentária

Em razão das regras previstas na LRF para o planejamento público, é obrigatória a elaboração de um demonstrativo da estimativa e compensação da renúncia de receita e da margem de expansão das despesas obrigatórias de caráter continuado. Esse demonstrativo é parte integrante do

Ano: 2015

Banca:

FCC

Órgão:

SEFAZ-PI

Prova:

FCC - 2015 - SEFAZ-PI - Analista do Tesouro Estadual - Conhecimentos Específicos |

Q476900

Administração Financeira e Orçamentária

Um dos principais instrumentos da transparência fiscal, que deve conter um comparativo com os limites relacionados às operações de crédito, inclusive por antecipação de receita, e que deverá ser assinado pelo controle interno, é o

Ano: 2015

Banca:

FCC

Órgão:

SEFAZ-PI

Prova:

FCC - 2015 - SEFAZ-PI - Analista do Tesouro Estadual - Conhecimentos Específicos |

Q476899

Administração Financeira e Orçamentária

Uma das funções do Analista do Tesouro Estadual é acompanhar e controlar as dívidas flutuantes e fundadas interna e externa do Estado do Piauí, devendo saber que integram a dívida fundada os

Ano: 2015

Banca:

FCC

Órgão:

SEFAZ-PI

Prova:

FCC - 2015 - SEFAZ-PI - Analista do Tesouro Estadual - Conhecimentos Específicos |

Q476898

Administração Financeira e Orçamentária

A transparência das contas públicas ganhou força com o advento da LRF. Tanto isso é fato que essa lei foi alterada justamente para o aprimoramento das regras de transparência. Uma dessas modificações foi a exigência de disponibilização a qualquer pessoa física ou jurídica de dados quanto à despesa pública, que deve ocorrer

Ano: 2015

Banca:

FCC

Órgão:

SEFAZ-PI

Prova:

FCC - 2015 - SEFAZ-PI - Analista do Tesouro Estadual - Conhecimentos Específicos |

Q476897

Administração Financeira e Orçamentária

A LRF dedicou atenção especial à renúncia de receitas e estabeleceu regras rígidas para sua realização. Nesse sentido, durante a execução do orçamento do Governo do Estado do Piauí ocorreram os seguintes fatos: 1 - anistia; 2 - remissão; 3 - concessão de isenção em caráter geral; 4 - subsídio; 5 - cancelamento de débito cujo montante era inferior ao do respectivo custo de cobrança. Configuram renúncia de receita os eventos de número